Learning Disability Week: Achieving dreams through personalised financial support

This Learning Disability Week, we are hearing from Abi* and how Dosh has supported her to use her money to do the things she has always wanted to do.

This week, 16 to 22 June, is Learning Disability Week! The theme this year is ‘Do You See Me’, which is about people with a learning disability being seen, heard and valued in society.

A huge part of this is people with a learning disability having control and independence over their money. For many of us, we use a bank account and money to pay for things without a second thought. However, people with a learning disability face additional barriers when accessing their money. This can be due to lack of accessible information, assumptions surrounding mental capacity or difficulty navigating the benefits system.

At Dosh, we support people with a learning disability use their money in the way they want and for the things they enjoy. We do this through our financial advocacy and appointeeship service. Each Financial Advocate supports people with benefits, budgeting, banking, and much more.

Abi’s* Story

Dosh has supported Abi for a while, and Abi calls her advocate her “money man.” Through Dosh’s support, she has been able to use her money to reach her goals.

In December 2024, she was able to book two tickets to see her favourite football team, Arsenal, play in the Women’s Super League! Abi’s support team helped her book the tickets, and her Dosh ‘money man’ ensured she had enough money to purchase them.

Abi got the train to the stadium and met lots of Arsenal fans on her journey. She was also able to buy herself a scarf and drinks bottle from the merchandise store. To top the day off, Arsenal Women’s won the match 4-0!

She has really enjoyed the day out and would love to go again, it was amazing!

Abi’s adventures didn’t stop there! She also was able to visit the Coronation Street TV studios. Abi asked if her support staff could contact her ‘money man’ to make sure it would be okay for her to go – of course it was!

Abi and her support team got to work and found a coach trip for her to go on which included an overnight hotel and dinner. The process was straightforward and before you knew it, Abi was on her trip to the cobbles.

Abi described the trip as:

The time of my life.

Abi’s support staff commented how supportive and approachable Dosh are to Abi. They feel like they can contact Dosh with any queries to ensure Abi achieves her dreams. Without the support from Dosh to help manage her finances, these trips could not be possible. Abi sends a huge thank you to her ‘money man’!

Everyone at Dosh are so pleased for Abi, and we are so proud of her Dosh support team who could help make these amazing moments happen. This demonstrates how vital it is that people with a learning disability and their support circles receive the right support when it comes to finances.

People with a learning disability deserve to use their money, their way. Just like everyone else.

To learn more about our support or make a referral, please get in touch with us through the contact form at the bottom of this page.

*Name has been changed for privacy reasons

Kelsey Cullen June 16th, 2025

Posted In: Learning Disability Week, News and Blogs, Stories

Tags: learning disability week

What does money mean to people with a learning disability?

Having access to money when you need it, enables us to live well at home, as well as get out and do the things we enjoy. However, people with a learning disability may need support with some aspects of their money, and so their experience of money and what it means to them may be different to others.

This is why in 2024, along with Thera Trust and the University of Bristol, we launched our Financial Wellbeing Project to find out how people with a learning disability feel about their money and what support they have with their finances.

Sam Holman and Gerard Starling were appointed as Co-Researchers of the project, with Sam having a lived experience of a learning disability. Gerard has a daughter with a learning disability and project manager experience at Thera. On his feelings on the project, Sam told us:

I care about the people I’m meeting and want them to have the best support. This is how Gerard and I have noticed that some the people we support don’t get a choice in terms of spending money. For example, saving up money to go on holiday. This is why this research is important.

Sam and Gerard held two workshops and individual interviews to understand people’s experiences. In total, they spoke to 16 individuals with a learning disability with interviews being up to an hour and a half long.

They asked people about 4 things:

- How they manage their money.

- Spending and saving.

- Support with benefits.

- How they generally feel about their finances.

Many people felt they had freedom over what they could spend but a common theme was the help they had from their support staff or family members. This meant that they didn’t feel as worried about managing their money or the impact of challenges like the cost-of-living crisis.

One person shared his experience of buying a pet gecko! His support team helped him visit the shop and learn how to look after a gecko, including ongoing costs. A family member then helped check affordability and arranged to get him the funds from the account they manage on his behalf.

The above findings and story demonstrate how important having the right support with finances is for people with a learning disability, whether that’s through existing support circles or an organisation like Dosh. However, most people didn’t talk about learning new skills around money and gaining more independence in future.

As a solution to this, Sam and Gerald felt that in the future it would be good to promote independence and control over money within people’s person-centred plans. For example, using person-centred active support approaches to gradually build people’s skills and options around money. This would help people to make their own decisions about what they do with their money, if they would like to.

From these reflections, we are looking at ways we can enable support teams and others to do this, in partnership with support providers and other organisations such as Thera and University of Bristol. We are always looking to improve and innovate our support for people with a learning disability and the project’s findings have been incredibly helpful.

If you want to read more about Sam and Gerald’s findings, you can view the report here. You can also watch back a webinar Sam held in April 2025 where he discussed his findings in more detail!

If you or someone you know with a learning disability would like support to have more financial independence, please get in touch with us using the contact form at the bottom of this page.

Together, we can support you to use your money, your way.

Kelsey Cullen May 14th, 2025

Posted In: News and Blogs, Sam, Thought pieces

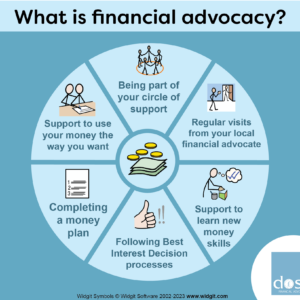

What is Financial Advocacy?

Dosh is unique in providing advocacy specifically around money, but many people don’t fully understand what a ‘Financial Advocate’ is or what we do day to day.

Advocacy in all its forms seeks to ensure that people, particularly those who are most vulnerable in society, are able to:

- Have their voice heard on issues that are important to them

- Defend and safeguard their rights

- Have their views and wishes genuinely considered when decisions are being made about their lives

Advocacy is the process of supporting and enabling people to:

- Express their views and concerns

- Access information and services

- Defend and promote their rights and responsibilities

- Explore choices and options’

At Dosh we focus our advocacy particularly around money, which is an area where people with a learning disability have in the past been given very little independence or control. We think that being able to use your money in the way you want is a key step to having control over the rest of your life.

A really important part of a financial advocates role is getting to know the people they support and listening to what they want. They do this by meeting regularly and taking the time when they meet to find out what is important to the people they support. Our financial advocates really enjoy getting to know a new person, learning how they like to communicate and becoming part of the team making sure they have a good life.

For some people, having someone outside of their family and day-to-day support team who is there just for them can be really empowering. Others might not be able to communicate or take part in every aspect of a decision, but their Dosh advocate can make sure that everyone who is important to them is involved in making big decisions so that we get the best possible option.

Dosh financial advocates know a huge amount about the benefits system, as well as other areas around personal finances such as money saving schemes and grants. Finances are an area where people can become nervous, wanting to safeguard and protect someone rather than give them real independence. At Dosh we help people build skills around finances, including budgeting, so that they can have more control over their money.

Some of the people we support find it very difficult to connect their short-term spending with long-term consequences, such as not paying their bills. We want to give people independence, but also make sure they are not at risk, so for these people we can transfer a small amount of money every day to their personal account.

This helps someone feel independent and can help them learn budgeting skills whilst still being sure that their rent will be paid and their savings will be kept safe.

Having a Financial Advocate gives people the opportunity and the space to think about the things they want and plan for the future.

Dosh financial advocates are not just administrators managing someone’s benefits, they are a part of their circle of support and want to help them to live a good life. Together with their family, support team and others who are important to them, Dosh can work to identify and reach their goals.

Kerry Measures August 8th, 2024

Posted In: News and Blogs

Delivering Dosh Money Awareness Training

Blog written by Steve Raw, Managing Director of Dosh

Sitting in the car park of the venue for today’s Money Awareness Training waiting for the caretaker to arrive, I am thinking about who I will meet and how the workshop will pan out during the course of the day. It is the feeling of excitement I always experience and is similar to the one I had a couple of weeks ago when I arrived for the training I would be delivering with a colleague in the Scottish Borders.

Whilst this is not my main employment (I am/have been the Managing Director of Dosh* since 2009), it is something I love doing and I think I can speak on behalf of my co-presenters, when I say that they love it too.

Introduction to the workshop and why

Several years ago, a support provider for people with a learning disability experienced some difficulties around their support with money. They had received a warning notice from a regulator that they needed to remedy this situation urgently. My organisation (Dosh Ltd – Financial Advocacy at www.dosh.org) became part of the solution by delivering workshops across the country for their managers and leaders. This is something we quickly found we enjoyed and, from the feedback we received from delegates, were good at it too. Since then, we have been providing our training across England and Scotland. (Not yet in Wales or Northern Ireland, but never say never!)

What the workshop includes:

- Concepts and Values – the support options around money for people we support

- Mental Capacity Act (MCA) 2005 and Best Interest Decisions

- Financial Safeguarding

- State Benefits Awareness

- Introduction to Banking and Banking options for people with a learning disability

- Budgeting, Money Planning, and the Dosh ‘Money Plan Game’

- And a Q & A about supporting people to be more independent and have more control over their money.

Each delegate receives a Money Awareness Workbook which includes information and resources.

Related. Dosh – Play the game featured in our workshop is an interactive a game which was specifically designed for people with a learning disability. Delegates also have an opportunity to play the paper version during our day together.

Delivering training to a team in Sutton in Cambridgeshire

Five things we can do:

- We can customise our workshop to fit the needs of your colleagues. Recently in Scotland an organisation wished to have a focus on Banking; in another part of the country, we were asked to include a presentation on ‘Safeguarding’.

- We make our training accessible for the people attending our workshops. Dosh delivers training to people with a learning disability, support teams, their managers, social workers, and finance teams

- We can deliver workshops anywhere in England, Scotland, and Wales

- Share our workshop presentation in a pdf after our training so that candidates do not need to worry about note taking during the session.

- We provide a follow-up service after the workshop.

What the day involves:

Chocolate! Yes, you read it correctly. We have an activity that you can actually eat and when your energy is beginning to sap, we come to the rescue with a liberal sharing of sweets.

We spend time getting to know our delegates, especially during the activities and the breaks. We find out what worries and challenges them and about supporting people with their money.

Working alongside our delegates as the workshop progresses.

We use a range of media and training methods including videos, film, power point, flip chart, paper exercises and Q & A sessions.

Five things that make us different?

- Financial Advocates who deliver the training also support people daily with their money and state benefits to bank, budget, and plan.

- I am a parent/carer for a woman with a learning disability who copes with autism, so I bring a family member’s perspective to the table.

- We share stories and experiences from our ‘day to day work’ to illustrate our presentations.

- We do not stick rigidly to our programme – if the class wants us to focus on a particular area during the day, we can adjust our programme.

- Our support and training do not end when the workshop finishes as we share our contact details with delegates so they can continue to request information and answer questions they may have thought of after the training.

Feedback from our recent workshops

“Very Informative” “Enjoyable, learning” “Nice and friendly speakers” “Friendly, nice speakers, learning enjoyable” “Enjoyable, easy to understand and interact” “It was spot on” “Very good well presented” “Enjoyable” “Enjoyed the day” “Good action points to take away” “Very good training session very informative” “Very informative and fun” “Valuable information and sweeties”

The best thing about today was: “Gaining more confidence around supporting people with their money” “I will, apply this to my work in the future”

If you would like to hear more about our training and would like to book a workshop, here are some of, out contact details

Information about our training: https://www.dosh.org/training-and-workshops-for-your-group-or-organisation/

email: Angela and Kerry [email protected]

email me: [email protected]

Note: * Dosh is a not-for-profit company, supporting adults with a learning disability to have more control and independence with their money, since 2007.

Kerry Measures March 31st, 2023

Posted In: Banking, News and Blogs, Stories

Planning for the Future

Many people who have a family member with a learning disability fear what will happen when they are no longer around to care for them.

This Blog covers some of the main things you can think about to help prepare for the future.

Planning for benefits and banking

Planning for benefits and banking

- If you manage the benefits of your relative with a learning disability as their appointee or deputy, it is important to plan for if you are no longer around or not able to get the money out.

- If you build a financial circle of support for your relative, their future will be more secure as they are not dependent on one person.

- A circle of support could include family, friends, support workers or other people who want to be part of the life of your relative.

Support

Support

- Some charities will support you to build a circle of support. They are listed below so you can find one local to you.

- You should also make sure that key people such as family members and support staff know important money information:

- Which bank are they with?

- How is this money accessed (PIN, signature, appointee)?

- Where are financial documents kept?

- You could also look for other support options, such as a financial advocacy or appointeeship service that could take over in the future.

Planning for financial security

Planning for financial security

- A Will is a written and legally binding document, which tells people what to do with money and property when you die.

- Anyone over 18 can make a Will if they have capacity.

- To have capacity they need to be able to answer ‘yes’ to the following questions:

- Do you know what a Will is?

- Do you know what things belong to you?

- Can you choose who gets your things after you die?

- If someone with a learning disability would like to make a Will, they should get written confirmation of their capacity from a solicitor and a medical professional before they make a Will.

- Wills are legally binding, but that does not mean they cannot be contested. It is important to seek legal advice when writing one.

- As well as a solicitor, you could also get support from an accountant or independent financial advisor.

Making a Will

Making a Will

- Most people never make a Will, but it is important to create one even if you do not have a lot of money.

- If you die without a Will, the law sets out how your assets will be divided (the Intestacy Rules).

- This may not be what you would have chosen.

- For many people, the main objectives of writing a Will are to:

- Name the person (an executor) who will be in charge of making sure your wishes are followed

- Pay off any money you owe

- Provide for your family and decide how you want your estate to be divided

- Create a secure financial future for a relative with a learning disability (a Discretionary Trust, see below)

- Ensure there is a guardian for children under 18

- Avoid delays, conflict or confusion

- You should involve your family and other people who are involved in your life in this process so that you can create a clear plan and help everyone to understand your wishes for the future.

- You should regularly review and update your Will to make sure it is still appropriate to your circumstances.

Creating a Discretionary Trust

- Many people with a learning disability are dependent on means-tested benefits, so they may lose some benefits and have to pay for their care costs if they inherit money directly.

- A Discretionary Trust can provide a structure to manage their money and protect their entitlement.

- A Trust is a legal arrangement set up by a solicitor. It states:

- Who can benefit from it (beneficiaries)

- Who can manage it (trustees)

- What the funds can be used for

- The beneficiaries could be a single relative with a learning disability, your extended family, or even a charity.

- A trustee must look after the assets of the Trust, and must spend the money in the best interests of the beneficiaries and in line with your wishes.

- You need to name at least two trustees in your Will. These should be people that you trust completely, and who are committed to the long-term responsibility of managing the Trust.

Resources and support

Creating a circle of support

Creating a circle of support

- Community Circles is a useful blog with information and advice www.communitycirclesblog.wordpress.com

- Circles Network is a national charity which can provide support in developing a circle of support and advocacy www.circlesnetwork.org.uk

- The Grapevine Help and Connect project specialises in bringing people together and helps people with a learning disability make connections www.grapevinecovandwarks.org

Finding a solicitor

Finding a solicitor

- The Disability Law Service can support you with finding a solicitor with experience of future planning for people with a learning disability www.dls.org.uk

- You can find a solicitor by calling the Law Society on 0870 606 5555 or on their website www.solicitors-online.com

- The Citizens Advice Bureau can advise you about solicitors near you. Call them on 08444 111 444 or visit your local office

- You will probably have to pay your solicitor, but you can get free legal advice with Legal Aid if you are over 70 or have a disability. Find out more by contacting Community Legal Advice on 0345 345 4345 or visit CommunityLegalAdvice.org.uk | Community Legal Advice

Where can I get more information?

Where can I get more information?

- Making a will www.gov.uk/make-will

- Information on trusts www.gov.uk/trusts-taxes

- Contact Dosh to discuss support options for your relative for the future, including financial advocacy and appointeeship for benefits.

Kerry Measures January 20th, 2023

Posted In: News and Blogs, Uncategorized

Mark’s Story

Earlier in the year, Mark expressed that wanted to replace his trike and discussed the idea with his Dosh Financial Advocate who suggested he visit a supplier for a suitable Trike to get some prices.

Whilst shopping around it became clear that he would not be able to fund this solely on his own, but over the year Mark managed to save just over half the amount by following the budget he had agreed with Dosh to give him some savings so he would have more choices.

Mark and Dosh also looked around for additional funding and following further discussions we put together a grant application to his care and support provider for financial assistance.

Before putting in the application, Mark and Dosh discussed this with everyone involved so we all knew what we needed to do to achieve his goal.

Mark then came up with the idea that he could use his new trike to do a sponsored bike ride and raise the funds to repay the grant. We added this proposal to the grant application, what an excellent idea!

Success! The grants team loved the idea of paying it forward and agreed to give Mark the funds he needed, so the trike was ordered and payment was arranged.

Now as you can see Mark is off and enjoying life on the road!

Kerry Measures December 6th, 2022

Posted In: News and Blogs, Stories

Banking Guide – Part 2

How can I get support with Banking?

1. Tell the bank what support and changes you need to help you. Build up a relationship with your local bank, so that they know you and what you need.

2. Ask what reasonable adjustments they can make, for example, to help you take money out of your account easily. Ask what they can do for people with a disability.

3. Ask the bank staff to check with their specialist disability team. They can give staff extra support and information.

4. Ask about the different types of accounts they have.

Remember the important laws:

• The Equality Act says people with a disability must get equal access to banking

• The Mental Capacity Act helps people make their own decisions and explains how to check someone’s capacity.

• Banking laws on identity, data protection and clear information.

| With Capacity | Without Capacity |

| Support (Reasonsable Adjustments) | Appointee Account |

| Third Party Mandate | Court of Protection – Single Decision |

| Joint Account | Court of Protection – Deputy |

| Basic Bank Account | Lasting Power of Attorney (If this was set up when you had capacity |

| Ordinary Power or Attorney | |

| Lasting Power or Attorney |

These accounts are slightly different with each bank.

They may have different names and work in different ways. Ask each bank to tell you what they have

How to deal with problems?

1. Ask them to explain their decision and what else they can do to help you.

2. Ask if they have a disability or customer services team that can help them or that you can talk to.

3. Speak to the manager in the bank.

4. Speak to the bank’s head office.

5. Make a formal complaint to the bank.

6. Report the problem to the Financial Ombudsman Service or Financial Conduct Authority.

7. Contact the Equality Advisory and Support Service helpline, Disability Law Service or Citizens Advice Bureau.

8. Think about taking the bank to court.

Kerry Measures October 10th, 2022

Posted In: Banking, News and Blogs, Stories

Being Bettina’s Dad – Being a Carer.

Being Bettina’s Dad – Being a Carer – A blog written by our Managing Director, Steve Raw.

This is Bettina. Bettina copes with autism and a learning disability.

Bettina is our pride and joy.

Dozing on the settee after a hard day’s work my pager started to beep. I woke up and phoned my transport department. They had the call that Joyce was going into labour, and they were sending a vehicle round to our flat to rush me to Berlin Military Hospital (BMH). We were 10 months into a two-year tour of occupied Berlin, and it was still a couple of years before the ‘Wall’ was to come down.

Within a couple of hours our beautiful daughter Bettina had come into our lives. It would be another 18 months before she was diagnosed with severe autism and a learning disability, but that didn’t matter to us (and still doesn’t) she is our beautiful daughter and love is enough. Being Bettina’s Dad: When love is not enough to keep you Safe and Secure – Leadership in the Raw

As I write this article, I have just received an invite from MacIntyre Families @MacFamilies https://www.macintyrecharity.org/ to be interviewed for a podcast. MacIntyre Families work with “all families ,siblings and circles of support to ensure voices are being heard, understood & importantly working together.”

So immediately I started thinking of the answers to potential questions and writing an article I could share which may help other carers and people who have an interest in supporting people.

Joyce and I are super organised and from the moment we got together we started planning. Having two daughters was always the plan, although I must admit that being a parent carer was not in the action plan.

“Most things don’t work out as expected but what happens instead often turns out to be the good stuff” Dame Judi Dench

On reflection, and 35 years of supporting Bettina, Dame Judi was quite right that it does indeed ‘turns out to be the good stuff’. ‘B’ as she is often referred to by her family, has enriched our lives and has taught us on what is important and what really is unimportant.

How has she done this?

Part 1. “Everybody has plans until they get hit for the first time”. Mike Tyson

1992 was not our family’s best year. Both my mum and father-in law passed away within weeks of each other; I had a severe bout of flu at the beginning of the year, and Bettina was permanently excluded from school halfway through her first term!

- “What doesn’t kill you makes you stronger” and those experiences drew us even closer together as a family knowing that we were dependant on each other and meant that we could bounce back and take on the world on behalf of Bettina.

- Money was super-tight at the time, as we had only just bought our first house and the interest rates skyrocketed to 15%, but we managed to find some money for a week in Great Yarmouth, our first holiday as a family – we still reminisce about that holiday – but we have found that when Bettina spends (intensive) time with her family on her hols she progresses at an increased rate, and she certainly did that year.

- With lots of teamwork, perseverance and love we got through 1992. Bettina quickly returned to school under its new leadership and enhanced provision.

Part 2. “Make up your mind that no matter what comes your way, no matter how difficult, no matter how unfair, you will do more than simply survive. You will thrive in spite of it.” —Joel Osteen

We thrived in spite of it:

- Joyce set up a support group for carers which morphed into a Carers Centre which also provided for Young Carers – the most vulnerable of carers.

- In 1996 on retirement from my Army career I started a new career in social care supporting adults with a learning disability. I am still thriving 26 years later as a Managing Director for Dosh dosh.org supporting adults with a learning disability to have more control and independence with their money.

- Over the last 30 years Bettina has brought laughter, fun and joy to her family. We have grown together while always keeping a sense of perspective thanks to ‘B’. I truly think there is nothing we can’t face as a family.

Part 3 – “I believe in being strong when everything seems to be going wrong. I believe that happy girls are the prettiest girls. I believe that tomorrow is another day and I believe in miracles.” Audrey Hepburn

Five fun things we get from being a carer for Bettina:

- As Bettina does not appear to have any concept of age both, Joyce and I are expected to function at the same energy level we did 30 years ago. I live a completely different life to the one my parents did at the age I am now.

- While Bettina’s verbal communication is limited, she does astound us sometimes with her opinions when she suddenly joins in the conversation at the dinner table. This often happens when I am pontificating about something. Bettina suddenly comments “I don’t care” which has us all falling about with laughter. A side eye from ‘B’ tells us she meant it.

- Bettina’s sayings and phrases are unique to her (‘B’ often creates new ones too) and she often expresses them in public – we know what they mean but fortunately the general public do not!

- Bettina gets us out of social engagements we don’t want to be part of. No extended family on Christmas day for us. “Bettina needs calm and quiet”

- Bettina helps us find and hold on to our “inner child” too easily lost when you become an adult: Being Bettina’s Dad: Finding your inner child and not forgetting to lose it – Leadership in the Raw

A quote for Bettina’s family and all carers:

“When written in Chinese the word “crisis” is composed of two characters – one represents danger and the other represents opportunity.”

Thank you, Bettina, for giving us a lifetime of opportunities.

Bettina with her big sister, Jennifer, and her dad.

Woolacombe Beach 2022

Picture courtesy of Joyce Raw (‘B’s tiger mum)

Kerry Measures July 27th, 2022

Posted In: News and Blogs, Uncategorized

Dosh Banking Guide Part One

In 2014, we created a report called Making Banking Easier. Our report highlighted some of the problems faced by people with a learning disability when banking.

It’s now 8 years since we published our report, and people with a learning disability still face many of the same challenges when banking. The advice we gave in the guide is still as important today as it was back then.

About Bank Accounts

Bank accounts are a way to look after and use your money through a bank or building society. Bank accounts are used for a lot of different things. You can put your money into your bank account, whether its from work or benefit payments. The money in your account can be used to pay bills and buy things you like. You can also keep money in your account to save for things for the future, like a holiday.

Banking

Banks can offer you a lot of different services. They can offer loans, mortgages and more. They also offer different types of bank account including Savings Accounts, Basic Bank Accounts, and Current Accounts.

If you have a bank account, your bank may write to you about the other services they offer. You should check carefully before you agree to anything new, and talk about any changes with a friend or advisor.

Getting a Bank account

You should be careful when signing up to a bank account or another banking service. You need to make sure you know what you are signing, how it will work, and how much it will cost you. Speak to someone you trust before you agree to anything with your bank.

Changing and closing your bank account

If you’re not happy with your bank account anymore, you should speak to your bank. They will be able to help you to close or change your account. It is easy to change or switch your bank account to one you would prefer. If you find an account you would like to switch to, speak to this bank who will help you switch from your old account.

Sometimes your bank will make a change to your account. If this happens, they will write to you to explain the changes they are making.

How can I get support with banking?

Whilst you don’t have to tell your bank about your disability, it can help if you tell them what adjustments and support you need. This could be physical if you require a wheelchair, or supporting you to understand the information the bank is giving you.

What should banks be doing?

- start by assuming that you have capacity.

- have different types of accessible information before you get a service (like advertising) and when you get the service (like in letters). They must tell you about these and make them available.

- support you to understand the information they give you.

- offer different ways of accessing a service and tell you about these. This should include internet and phone services.

- have branches that you can visit. Some banks have a branch near you, or let you use their services through the Post Office.

- accept different things as proof of identity. They can tell you what different things they accept as proof.

- judge someone’s capacity to make a decision by following the Mental Capacity Act, if they are worried or unsure about someone’s capacity.

- explain why they will not give you a service or how they have decided that you do not have capacity.

- aim to use the least restrictive option for people who lack capacity.

- offer each person the best access to banking for them. This could include different types of bank accounts that can be used with support if someone does not have the capacity to manage a bank account by themselves.

With Capacity

If you have the capacity to manage a bank account but still want some support, there are different things you can do, including:

Support from your bank: Banks can give you different types of support. For example, they can give you a chip and signature card, instead of a chip and PIN card. A PIN is a secret 4-digit number you usually have to remember to use your card.

They can give you information in different formats (like Easy Read) and they can explain things to you if they are hard to understand.

Third party mandate: You give another person temporary access to your bank account. The bank will have a form to let you do this.

Joint account: You share a bank account with another person and you both have full access to the money.

Basic bank account: You have your own bank account but it has some limits on what it can do. The details are different between the different banks.

They are for people with a low credit score, people that do not want an overdraft and people that want to limit how much they can spend and reduce the risks and costs of having a bank account.

Ordinary Power of Attorney: You give someone else control over all or part of your money and finances. This will stop if you lose capacity.

Lasting Power of Attorney for property and financial affairs: You give someone power over your money and finances when you still have capacity.

They can help you manage your money if you would like them to, even if you have capacity to do so yourself

Without capacity

Appointee account: Your appointee (the person or group that manages your benefits for you) has a separate account for your benefit money (like the Dosh Client Account).

Lasting Power of Attorney for property and financial affairs: You give someone power over your money and finances when you still have capacity.

Later, when you lose capacity to look after your own money, your attorney can step in and manage your money and property for you.

Court of Protection decision: This is usually for a one-off or single decision, for example the court decides to let someone else sign a tenancy agreement for a house for you.

Court of Protection Deputy for property and financial affairs: The court decides to appoint someone (your deputy) who can make decisions about your money for you, if you cannot make those decisions yourself.

Your deputy must work hard to support you to make decisions about your money yourself. The deputy must only step in and make a decision for you, if you cannot make that decision, even with lots of help and support.

If you are interested in these options, speak to your bank to find out what they can offer you. The details of each account will be different between banks and it is a good idea to ask what other options they offer.

Remember, make sure you understand all the information about any banking service before you sign up for it.

If you want more information about making legal changes like power of attorney or the Court of Protection, visit the gov.uk website

Edward Goater July 17th, 2022

Posted In: Banking, News and Blogs